Arrow ECS wants to be seen by its resellers and MSPs as an ‘as-a-service partner’, its UKI boss said as he opened up on his 2026 priorities.

Part of NYSE-listed Arrow Electronics, Arrow ECS is the world’s third-largest IT distributor behind TD Synnex and Ingram, with 2024 gross billings of $7.9bn.

Boasting offices in Dublin, Harrogate and Newmarket, it ranked fifth in Oxygen’s 50 UK Must-Know Distributors and Marketplaces 2025.

“Well on our way to becoming that as-a-service partner”

Talking to IT Channel Oxygen, UK&I Regional Director Anthony Dobson said the VAD is on a mission to add more “pockets of value” beyond its traditional value distribution business.

“There’s this thing that distributors don’t want to be called ‘distributors’ anymore,” he said.

“The reality is that value distribution is still important. It’s still key: Do you have scale? Do you reach thousands of partners? Do you stock? Do you price? Do you deliver?

“But the value of that as a go to market is diminishing all the time. Therefore, you’ve got to create other pockets of value that keep you relevant with the vendors, the ecosystem and the downstream customers.

“The next evolution for us was how do we become an aggregation partner?

“And the next evolution of that, which we’re well on the way through now, is being seen as an as-a-service partner.”

This next phase will see Arrow ECS help with customer self-serve engines and offer “complementary partner services”, Dobson explained.

“These either make the smaller partners feel bigger and more equipped or, with the bigger partners, allow them to put their expensive services people on high-margin things and we help with some of the more menial services,” he said.

“Because of the investments we’ve made in things like ArrowSphere and AI Labs, I feel that we’re well along the way to becoming that as-a-service partner.”

“We’re perfectly aligned to help”

Arrow ECS President Eric Nowak acknowledged on a Q3 earnings call that the distributor is encountering “growing pains” in its efforts to pursue more ‘strategic outsourcing’ pacts with vendors.

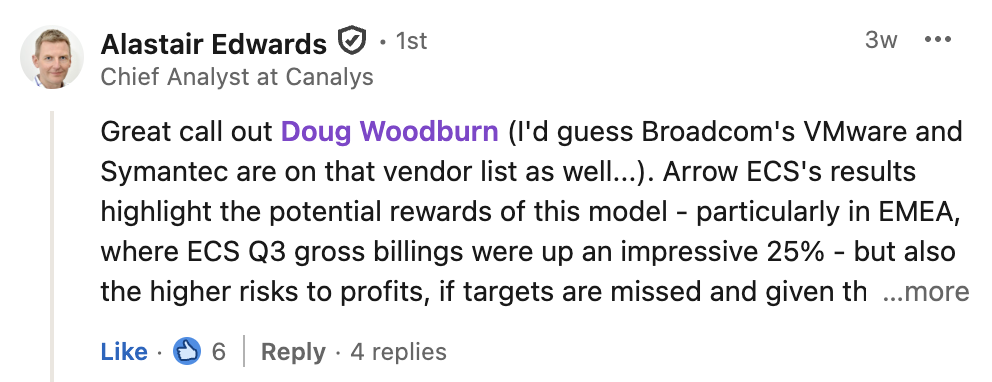

It has already achieved this with “multiple large suppliers”, thought to include Citrix, Broadcom and Symantec (see LinkedIn comment from Omdia Chief Analyst Alastair Edwards below).

Despite taking a $21m charge on these contracts in its most-recent quarter, the NYSE-listed outfit is convinced they will eventually yield double the gross margins it achieves in the rest of ECS.

“It’s not a model per sae,” Dobson said of the new sole-supplier push.

“A vendor may be struggling to penetrate the commercial market, or there may be countries where they can’t afford to invest in having big premises and people.

“We believe distribution, and Arrow in particular, are perfectly aligned because of their scale and investments to go help within that market.”

“It’s no secret”

Dobson picked out maximising Arrow ECS’ core business and traditional vendor relationships as one of three key priorities for the UK&I business 2026.

“If you look at how vendors reward distribution, there’s absolutely no secret in the fact that they want us to recruit and drive more mid-tier partners,” he explained.

“We’ve seen the vendors have pivoted to some of their bigger partners and customers, and they need distribution to drive what I would call the managed space – internally we call it midmarket.”

Cloud and partner services complete Dobson’s priority list.

“You can only look to the future if you’re growing that traditional business,” he said.

The term ‘distributor’ has come under scrutiny in 2025 as the likes of Ingram and Pax8 aggressively position themselves as platforms or marketplaces (see here and here).

“Distribution as a word is okay for me, but for me there’s got to be an understanding that it’s only a part of what we do,” Dobson said.

“It’s an essential part, but we then scale out and build from that.”

Doug Woodburn is editor of IT Channel Oxygen